This article sets out the requirements for setting a complete emissions boundary for your organisation.

Setting your organisation emissions boundary involves the following steps:

Introduction

Establishing a greenhouse gas (GHG) emissions boundary is a critical step for organisations to effectively measure and manage their GHG emissions.

The GHG Protocol approach provides a standardised framework for establishing a GHG emissions boundary that can be used by organisations of all types and sizes.

This article will provide a step-by-step guide for Pathzero Clarity users to establish a GHG emissions boundary using the GHG Protocol approach.

Step 1: Identify organisational boundaries

Organisational boundaries define the physical and operational limits of an organisation, and identifying them is the first step in establishing a GHG emissions boundary.

There are three types of organisational boundary approaches:

- Operational control

- Financial control

- Equity share

The most common approach uses the operational control approach, which includes all the activities and processes that an organisation has direct control over.

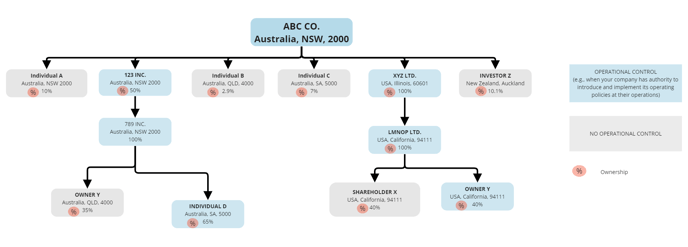

To identify the organisational boundary, Pathzero requires the organisations to provide their legal entity structure including international business numbers (ABN in Australia), and the operational activities of each legal entity.

Please provide a copy of your entity structure to Pathzero to allow our sustainability consultants to confirm the organisational boundary.

The figure below shows an example of an entity structure with operational control determined across subsidiaries.

Step 2: Identify operational boundaries

Once the organisational boundaries have been identified, the next step is to determine which activities and processes the organisation has operational control over.

Operational control refers to the ability to direct the policies and management of an activity or process, and it is used to define the GHG emissions sources that are included in the GHG emissions boundary.

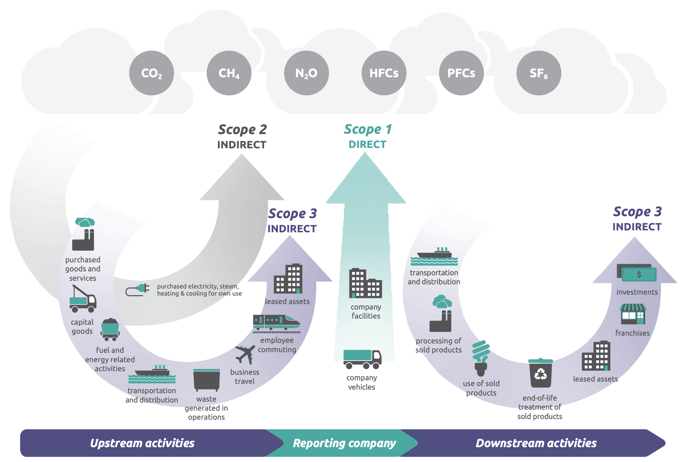

Step 3: Determine scope 1, scope 2, and scope 3 emissions

Once the operational boundary has been established, the next step is to determine the GHG emissions sources that fall within each of the three GHG Protocol scopes: scope 1, scope 2, and scope 3.

- Scope 1 emissions are direct emissions from sources that are owned or controlled by the organisation, such as combustion of fossil fuels.

- Scope 2 emissions are indirect emissions from the generation of purchased electricity, heat, or steam.

- Scope 3 emissions are all other indirect emissions that occur as a result of an organisation's activities, such as emissions from the transportation of goods or services.

Overview of GHG Protocol scopes and emissions across the value chain

Source: GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (PDF, p5), World Resources Institute and WBCSD.

Step 4: Define GHG emissions boundary

With the GHG emissions sources identified, the next step is to define the GHG emissions boundary.

The GHG emissions boundary is the boundary that encompasses all GHG emissions sources that are included in the organisation's inventory.

The GHG Protocol approach requires organisations to include all scope 1 and scope 2 emissions, and relevant scope 3 emissions categories based on the relevance test.

Any exclusions based on the relevance test need to be disclosed and justified.

Note that scope 3 emissions are an important consideration to achieve decarbonisation across the economy, as organisations can exert their influence across their value chain to achieve decarbonisation outcomes.